Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9

Draft Ok to Print

AH XSL/XML

Fileid: … ions/i2555/2023/a/xml/cycle04/source (Init. & Date) _______

Page 1 of 9 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2023

Instructions for Form 2555

Foreign Earned Income

Department of the Treasury

Internal Revenue Service

Section references are to the Internal Revenue Code unless

otherwise noted.

Future Developments

For the latest information about developments related to Form

2555 and its instructions, such as legislation enacted after they

were published, go to

IRS.gov/Form2555.

What's New

Exclusion amount. For 2023, the maximum exclusion amount

has increased to $120,000.

Reminder

Tax home for individuals serving in a combat zone. Certain

individuals serving in a combat zone in support of the U.S.

Armed Forces may nonetheless establish a tax home in the

foreign country of the combat zone. For more information, see

Tax home test under Who Qualifies, later.

General Instructions

Don't include on Form 1040 or 1040-SR, line 25a or 25b

(federal income tax withheld from Form(s) W-2 or 1099,

respectively), any taxes an employer withheld from your

pay that were paid to the foreign country's tax authority instead

of the U.S. Treasury.

Purpose of Form

If you qualify, you can use Form 2555 to figure your foreign

earned income exclusion and your housing exclusion or

deduction. You cannot exclude or deduct more than the amount

of your foreign earned income for the year.

General Information

If you are a U.S. citizen or a resident alien living in a foreign

country, you are subject to the same U.S. income tax laws that

apply to U.S. citizens and resident aliens living in the United

States.

Note. Specific rules apply to determine if you are a resident or

nonresident alien of the United States. See Pub. 519.

Foreign country. A foreign country is any territory under the

sovereignty of a government other than that of the United States.

The term “foreign country” includes the country's territorial

waters and airspace, but not international waters and the

airspace above them. It also includes the seabed and subsoil of

those submarine areas adjacent to the country's territorial waters

over which it has exclusive rights under international law to

explore and exploit the natural resources.

The term “foreign country” doesn't include U.S. territories. It

doesn't include the Antarctic region.

Who Qualifies

You qualify to exclude your foreign earned income from gross

income if both of the following apply.

•

You meet the tax home test (discussed later).

•

You meet either the bona fide residence test or the physical

presence test (discussed later).

CAUTION

!

Note.

Income from working abroad as an employee of the U.S.

Government does not qualify for either of the exclusions or the

housing deduction. Don't file Form 2555.

Tax home test. To meet this test, your tax home must be in a

foreign country, or countries (see Foreign country, earlier),

throughout your period of bona fide residence or physical

presence, whichever applies. For this purpose, your period of

physical presence is the 330 full days during which you were

present in a foreign country, or countries, not the 12 consecutive

months during which those days occurred.

Note. If you did not live 330 full days in a foreign country, or

countries, during a 12-month period, you are not entitled to claim

the foreign earned income exclusion. The 330 qualifying days do

not have to be consecutive.

Your tax home is your regular or principal place of business,

employment, or post of duty, regardless of where you maintain

your family residence. If you don't have a regular or principal

place of business because of the nature of your trade or

business, your tax home is your regular place of abode (the

place where you regularly live).

You aren't considered to have a tax home in a foreign country

for any period during which your abode is in the United States,

unless you are serving in support of the U.S. Armed Forces in an

area designated as a combat zone. See Service in a combat

zone, later. Otherwise, if your abode is in the United States, you

will not meet the tax home test and cannot claim the foreign

earned income exclusion.

The location of your abode is based on where you maintain

your family, economic, and personal ties. Your abode is not

necessarily in the United States merely because you maintain a

dwelling in the United States, whether or not your spouse and

dependents use the dwelling. Your abode is not necessarily in

the United States while you are temporarily in the United States.

However, these factors can contribute to your having an abode in

the United States.

Example. You are employed on an offshore oil rig in the

territorial waters of a foreign country and work a 28-day on/

28-day off schedule. You return to your family residence in the

United States during your off periods. You are considered to

have an abode in the United States and don't meet the tax home

test. You can't claim either of the exclusions or the housing

deduction.

Service in a combat zone. Citizens or residents of the

United States serving in an area designated by the President of

the United States by Executive order as a combat zone for

purposes of section 112 in support of the U.S. Armed Forces can

qualify as having a tax home in a foreign country, even if they

have an abode within the United States. For a list of

IRS-recognized combat zones, go to

IRS.gov/Newsroom/

Combat-Zones.

Travel to Cuba

Generally, if you were in Cuba in violation of U.S. travel

restrictions, the following rules apply.

•

Any time spent in Cuba can't be counted in determining if you

qualify under the bona fide residence or physical presence test.

•

Any income earned in Cuba isn't considered foreign earned

income.

Oct 16, 2023

Cat. No. 11901A

Page 2 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

Any housing expenses in Cuba (or housing expenses for your

spouse or dependents in another country while you were in

Cuba) aren't considered qualified housing expenses.

Note. If you performed services at the U.S. Naval Base at

Guantanamo Bay, you were not in violation of U.S. travel

restrictions.

Waiver of Time Requirements

If your tax home was in a foreign country and you were a bona

fide resident of, or physically present in, a foreign country and

had to leave because of war, civil unrest, or similar adverse

conditions, the minimum time requirements specified under the

bona fide residence and physical presence tests may be waived.

You must be able to show that you could have reasonably

expected to meet the minimum time requirements if you hadn't

been required to leave. Each year, the IRS will publish in the

Internal Revenue Bulletin a list of the only countries that qualify

for the waiver for the previous year and the dates they qualify. If

you left one of the countries during the period indicated, you can

claim the tax benefits on Form 2555, but only for the number of

days you were a bona fide resident of, or physically present in,

the foreign country.

If you can claim either of the exclusions or the housing

deduction because of the waiver of time requirements, attach a

statement to your return explaining that you expected to meet the

applicable time requirement, but the conditions in the foreign

country prevented you from the normal conduct of business.

Also, enter “Claiming Waiver” in the top margin on page 1 of

Form 2555.

Additional Information

Pub. 54 has more information about the bona fide residence test,

the physical presence test, the foreign earned income exclusion,

and the housing exclusion and deduction. You can download this

publication (as well as other forms and publications) at IRS.gov/

Forms.

When To File

A 2023 calendar year Form 1040 or 1040-SR is generally due

April 15, 2024.

However, you are automatically granted a 2-month extension

of time to file (to June 15, 2024, for a 2023 calendar year return)

if, on the due date of your return, you live outside the United

States and Puerto Rico and your

tax home (defined earlier) is

outside the United States and Puerto Rico. If you take this

extension, you must attach a statement to your return explaining

that you meet these two conditions.

The automatic 2-month extension also applies to paying the

tax. However, you will owe interest on any tax not paid by the

regular due date of your return.

When to claim the exclusion(s). The first year you plan to

take the foreign earned income exclusion and/or the housing

exclusion or deduction, you may not yet have met either the

physical presence test or the bona fide residence test by the due

date of your return (including the automatic 2-month extension,

discussed earlier). If this occurs, you can either:

1. Apply for a special extension to a date after you expect to

qualify, or

2. File your return timely without claiming the exclusion and

then file an amended return after you qualify.

Special extension of time. To apply for this extension,

complete and file Form 2350 with the Department of the

Treasury, Internal Revenue Service Center, Austin, TX

73301-0045, before the due date of your return. Interest is

charged on the tax not paid by the regular due date as explained

earlier.

Amended return.

File Form 1040-X to change a return you

have already filed. Generally, Form 1040-X must be filed within 3

years after the date the original return was filed or within 2 years

after the date the tax was paid, whichever is later.

Where To File

Attach Form 2555 to Form 1040 or 1040-SR when filed. Mail

your Form 1040 or 1040-SR to one of the special addresses

designated for those filing Form 2555. Do not mail your Form

1040 or 1040-SR to the addresses associated with your state of

residence if Form 2555 is attached. See the Instructions for Form

1040. The filing addresses are also available at

IRS.gov/Filing/

International-Where-To-File-Form-1040-Addresses-for-

Taxpayers-and-Tax-Professionals.

Choosing the Exclusion(s)

To choose either of the exclusions, complete the appropriate

parts of Form 2555 and file it with your Form 1040, 1040-SR, or

1040-X. Your initial choice to claim the exclusion must usually be

made on a timely filed return (including extensions) or on a

return amending a timely filed return. However, there are

exceptions. See

Pub. 54 for details.

Once you choose to claim the exclusion(s), that choice

remains in effect for that year and all future years unless it is

revoked. To revoke your choice, you must attach a statement to

your return for the first year you don't wish to claim the

exclusion(s). If you revoke your choice, you can't claim the

exclusion(s) for your next 5 tax years without the approval of the

IRS. See

Pub. 54 for more information.

Note. It is not necessary to affirmatively revoke your choice if

you don’t have any foreign earned income.

Additional child tax credit. You can't take the additional child

tax credit if you claim either of the exclusions or the housing

deduction.

Earned income credit. You can't take the earned income credit

if you claim either of the exclusions or the housing deduction.

Foreign tax credit or deduction. You can't take a credit or

deduction for foreign income taxes paid or accrued on income

that is excluded under either of the exclusions. If all of your

foreign earned income is excluded, you can't claim a credit or

deduction for the foreign taxes paid or accrued on that income. If

only part of your income is excluded, you can't claim a credit or

deduction for the foreign taxes allocable to the excluded income.

See

Pub. 514 for details on how to figure the amount allocable to

the excluded income.

IRA deduction. If you claim either of the exclusions, special

rules apply in figuring the amount of your IRA deduction. For

details, see

Pub. 590-A.

Figuring Tax on Income Not Excluded

If you claim either of the exclusions or the housing deduction,

you must figure the tax on your nonexcluded income using the

tax rates that would have applied had you not claimed the

exclusions. See the Instructions for Form 1040 and complete the

Foreign Earned Income Tax Worksheet to figure the amount of

tax to enter on Form 1040 or 1040-SR, line 16. When figuring

your alternative minimum tax on Form 6251, you must use the

Foreign Earned Income Tax Worksheet in the Instructions for

Form 6251.

-2-

Instructions for Form 2555 (2023)

Page 3 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Specific Instructions

Part I

Line 1. Enter your entire address, including city or town, state or

province, country, and ZIP or foreign postal code. If using a

military or diplomatic address, include the country in which you

are living or stationed.

Line 9. Enter your tax home(s) and date(s) established. See Tax

home test under Who Qualifies, earlier.

You must complete either Part II or Part III of Form 2555,

but not both parts.

Part II

Bona Fide Residence Test

To meet this test, you must be one of the following.

•

A U.S. citizen who is a bona fide resident of a foreign country,

or countries, for an uninterrupted period that includes an entire

tax year (January 1–December 31, if you file a calendar year

return).

•

A U.S. resident alien who is a citizen or national of a country

with which the United States has an income tax treaty in effect

and who is a bona fide resident of a foreign country, or countries,

for an uninterrupted period that includes an entire tax year

(January 1–December 31, if you file a calendar year return). See

Table 3 at

IRS.gov/Individuals/International-Taxpayers/Tax-

Treaty-Tables for a list of countries with which the United States

has an income tax treaty in effect.

Whether you are a bona fide resident of a foreign country

depends on your intention about the length and nature of your

stay. Evidence of your intention may be your words and acts. If

these conflict, your acts carry more weight than your words.

Generally, if you go to a foreign country for a definite, temporary

purpose and return to the United States after you accomplish it,

you aren't a bona fide resident of the foreign country. If

accomplishing the purpose requires an extended, indefinite stay,

and you make your home in the foreign country, you may be a

bona fide resident. See

Pub. 54 for more information and

examples.

Line 10. Enter the dates your bona fide residence began and

ended. If you are still a bona fide resident, enter “Continues” in

the space for the date your bona fide residence ended.

Lines 12a and 12b. If you check “Yes” on line 12a, enter the

type(s) of family member(s) and the date(s) they lived with you

on line 12b. Acceptable entries for family members on line 12b

include child, foster child, grandchild, parent, grandparent,

brother, sister, aunt, uncle, nephew, niece, son, daughter,

spouse, or other. If you check “No” on line 12a, leave line 12b

blank or enter “None.”

Lines 13a and 13b. If you submitted a statement of

nonresidence to the authorities of a foreign country in which you

earned income and the authorities hold that you aren't subject to

their income tax laws by reason of nonresidency in the foreign

country, you aren't considered a bona fide resident of that

country.

If you submitted such a statement and the authorities haven't

made an adverse determination of your nonresident status, you

aren't considered a bona fide resident of that country.

CAUTION

!

Part III

Physical Presence Test

To meet this test, you must be a U.S. citizen or resident alien who

is physically present in a foreign country, or countries, for at least

330 full days during any period of 12 months in a row. A full day

means the 24-hour period that starts at midnight.

To figure 330 full days, add all separate periods you were

present in a foreign country during the 12-month period shown

on line 16. The 330 full days can be interrupted by periods when

you are traveling over international waters or are otherwise not in

a foreign country. See Pub. 54 for more information and

examples.

Note. A nonresident alien who, with a U.S. citizen or U.S.

resident alien spouse, chooses to be taxed as a resident of the

United States can qualify under this test if the time requirements

are met. See Pub. 54 for details on how to make this choice.

Line 16. The 12-month period on which the physical presence

test is based must include 365 days, part of which must be in

2023. The dates may begin or end in a calendar year other than

2023.

You must enter dates in both spaces provided on line 16.

Don't enter “Continues” in the space for the ending date.

Part IV

Foreign Earned Income

Enter in this part the total foreign earned income you earned and

received (including income constructively received) during the

tax year. If you are a cash basis taxpayer, include in income on

Form 1040 or 1040-SR the foreign earned income you received

during the tax year regardless of when you earned it. (For

example, include wages from Form 1040 or 1040-SR, line 1.)

Income is earned in the tax year you perform the services for

which you receive the pay. But if you are a cash basis taxpayer

and, because of your employer's payroll periods, you received

your last salary payment for 2022 in 2023, that income may be

treated as earned in 2023. If you cannot treat that salary

payment as income earned in 2023, the rules explained under

Income earned in prior year, later, apply. See Pub. 54 for more

details.

Foreign earned income for this purpose means wages,

salaries, professional fees, and other compensation received for

personal services you performed in a foreign country during the

period for which you meet the tax home test and either the bona

fide residence test or the physical presence test. It also includes

noncash income (such as a home or car) and allowances or

reimbursements.

Foreign earned income doesn't include amounts that are

actually a distribution of corporate earnings or profits rather than

a reasonable allowance as compensation for your personal

services.

Foreign earned income also doesn't include the following

types of income.

•

Pension and annuity income (including social security benefits

and railroad retirement benefits treated as social security).

If you receive a pension from your employment abroad

and don't need a social security agreement between the

United States and your country of residence to qualify for

retirement benefits in either country, the amount of your U.S.

benefit may be affected. This is a result of a condition in U.S.

Social Security law called the Windfall Elimination Provision

TIP

CAUTION

!

Instructions for Form 2555 (2023)

-3-

Page 4 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

(WEP). For more information about the WEP, go to SSA.gov/

International/WEP_Intro.html.

•

Interest, ordinary dividends, capital gains, alimony, etc.

•

Amounts paid to you by the U.S. Government or any of its

agencies if you were an employee of the U.S. Government or any

of its agencies.

•

Amounts received after the end of the tax year following the

tax year in which you performed the services.

•

Amounts you must include in gross income because of your

employer’s contributions to a nonexempt employees’ trust or to a

nonqualified annuity contract.

Income received in prior year. Foreign earned income

received in 2022 for services you performed in 2023 can be

excluded from your 2022 gross income if, and to the extent, the

income would have been excludable if you had received it in

2023. To claim the additional exclusion, you must amend your

2022 tax return. To do this, file Form 1040-X.

Income earned in prior year. Foreign earned income received

in 2023 for services you performed in 2022 can be excluded

from your 2023 gross income if, and to the extent, the income

would have been excludable if you had received it in 2022.

If you are excluding income under this rule, do not include this

income in Part IV. Instead, attach a statement to Form 2555

showing how you figured the exclusion. Enter the amount that

would have been excludable in 2022 on Form 2555 to the left of

line 45. Next to the amount, enter “Exclusion of Income Earned

in 2022.” Include it in the total reported on line 45.

Note. If you claimed any deduction, credit, or exclusion on your

2022 return that is definitely related to the 2022 foreign earned

income you are excluding under this rule, you may have to

amend your 2022 income tax return to adjust the amount you

claimed. To do this, file Form 1040-X.

Line 20. If you engaged in an unincorporated trade or business

in which both personal services and capital were material

income-producing factors, a reasonable amount of

compensation for your personal services will be considered

earned income. The amount treated as earned income, however,

can't be more than 30% of your share of the net profits from the

trade or business after subtracting the deduction for the

employer-equivalent portion of self-employment tax.

If capital is not an income-producing factor and personal

services produced the business income, the 30% rule does not

apply. Your entire gross income is earned income.

Line 23. List other foreign earned income not included on lines

19 through 22. You can enter “Various” on the dotted lines to the

left of the entry space if you have other foreign earned income

from multiple sources.

Line 25. Enter the value of meals and/or lodging provided by, or

on behalf of, your employer that is excludable from your income

under section 119. To be excludable, the meals and lodging

must have been provided for your employer's convenience and

on your employer's business premises. In addition, you must

have been required to accept the lodging as a condition of your

employment. If you lived in a camp provided by, or on behalf of,

your employer, the camp may be considered part of your

employer's business premises. See

Exclusion of Meals and

Lodging in Pub. 54 for details.

Part VI

Line 28. Enter the total reasonable expenses paid or incurred

during the tax year by you, or on your behalf, for your foreign

housing and the housing of your spouse and dependents if they

lived with you. You can also include the reasonable expenses of

a second foreign household (defined later). Housing expenses

are considered reasonable to the extent they aren't lavish or

extravagant under the circumstances.

Housing expenses include rent, utilities (other than telephone

charges), real and personal property insurance, nonrefundable

fees paid to obtain a lease, rental of furniture and accessories,

residential parking, and household repairs. You can also include

the fair rental value of housing provided by, or on behalf of, your

employer if you haven't excluded it on line 25.

Don't include deductible interest and taxes, any amount

deductible by a tenant-stockholder in connection with

cooperative housing, the cost of buying or improving a house,

principal payments on a mortgage, or depreciation on the house.

Also, don't include the cost of domestic labor, pay television, or

buying furniture or accessories.

Include expenses for housing only during periods for which:

•

The value of your housing isn't excluded from gross income

under section 119 (unless you maintained a second foreign

household, as defined later), and

•

You meet the tax home test and either the bona fide residence

or physical presence test.

Second foreign household. If you maintained a separate

foreign household for your spouse and dependents at a place

other than your tax home because the living conditions at your

tax home were dangerous, unhealthful, or otherwise adverse,

you can include the expenses of the second household on

line 28.

Married couples. The following rules apply if both you and your

spouse qualify for the tax benefits of Form 2555.

Same foreign household. If you and your spouse lived in the

same foreign household and file a joint return, you must figure

your housing amounts (line 33) jointly. If you file separate returns,

only one spouse can claim the housing exclusion or deduction.

In figuring your housing amount jointly, either spouse (but not

both) can claim the housing exclusion or housing deduction.

However, if you and your spouse have different periods of

residence or presence, and the one with the shorter period of

residence or presence claims the exclusion or deduction, you

can claim as housing expenses only the expenses for that

shorter period. The spouse claiming the exclusion or deduction

can aggregate the housing expenses of both spouses, subject to

the limit on housing expenses (line 29b), and subtract his or her

base housing amount.

Separate foreign households. If you and your spouse lived

in separate foreign households, you each can claim qualified

expenses for your own household only if:

•

Your tax homes weren't within a reasonable commuting

distance of each other, and

•

Each spouse's household wasn't within a reasonable

commuting distance of the other spouse's tax home.

Otherwise, only one spouse can claim his or her housing

exclusion or deduction. This is true even if you and your spouse

file separate returns.

See Pub. 54 for additional information.

Line 29a. Enter the city or other location (if applicable) and the

country where you incurred foreign housing expenses during the

tax year only if your location is listed in the table at the end of

these instructions; otherwise, leave this line blank.

Line 29b. Your housing expenses may not exceed a certain

limit. The limit on housing expenses varies depending upon the

location in which you incur housing expenses. In 2023, for most

locations, this limit is $36,000 (30% of $120,000) if your

qualifying period includes all of 2023 (or $98.63 per day if the

number of days in your qualifying period that fall within your 2023

tax year is less than 365). Eligible housing amounts for exclusion

and deduction are updated yearly and available at

IRS.gov/irb/

2023-13_IRB#NOT-2023-26.

-4-

Instructions for Form 2555 (2023)

Page 5 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Housing expense limits are based on geographic differences

in foreign housing costs relative to housing costs in the United

States. They are updated on a yearly basis and are available at

IRS.gov/irb/2023-13_IRB#NOT-2023-26. If the location in which

you incurred housing expenses is listed in the table, or the

number of days in your qualifying period that fall within the 2023

tax year is less than 365, use the Limit on Housing Expenses

Worksheet—Line 29b to figure the amount to enter on line 29b. If

the location in which you incurred housing expenses is not listed

in the table, and the number of days in your qualifying period is

365, enter $36,000 on line 29b.

Example. For 2023, because your location is not listed in the

table at the end of the instructions, your limit on housing

expenses is $98.63 per day. If you file a calendar year return and

your qualifying period is January 1, 2023, to October 3, 2023

(276 days), you would enter $27,222 on line 29b ($98.63

multiplied by 276 days).

Election to apply higher limit on housing expenses. For

2022, you could elect to apply the 2023 limits on housing

expenses as discussed in section 4 of Notice 2023-26, available

at IRS.gov/irb/2023-13_IRB#NOT-2023-26.

The IRS and the Treasury Department anticipate that you will

also be allowed to make an election to apply the 2024 limits to

figure your 2023 limit on housing expenses. The authorization to

make the election will be provided in a future annual notice

published in the Internal Revenue Bulletin.

More than one foreign location. If you moved during the

2023 tax year and incurred housing expenses in more than one

foreign location as a result, complete the Limit on Housing

Expenses Worksheet—Line 29b for each location in which you

incurred housing expenses, entering the number of qualifying

days during which you lived in the applicable location on line 1.

Add the results shown on line 4 of each worksheet, and enter the

total on line 29b.

If you moved during the 2023 tax year and are

completing more than one Limit on Housing Expenses

Worksheet—Line 29b, the total number of days entered

on line 1 of your worksheets may not exceed the total number of

days in your qualifying period that fall within the 2023 tax year

(that is, the number of days entered on Form 2555, line 31).

CAUTION

!

Line 31. Enter the number of days in your qualifying period that

fall within your 2023 tax year. Your qualifying period is the period

during which you meet the tax home test and either the bona fide

residence or physical presence test.

Example. You establish a tax home and bona fide residence

in a foreign country on August 14, 2023. You maintain the tax

home and residence until January 31, 2025. You are a calendar

year taxpayer. The number of days in your qualifying period that

fall within your 2023 tax year is 140 (August 14 through

December 31, 2023).

Nontaxable U.S. Government allowances. If you or your

spouse received a nontaxable housing allowance as a military or

civilian employee of the U.S. Government, see

Pub. 54 for

information on how that allowance may affect your housing

exclusion or deduction.

Line 34. Enter any amount your employer paid or incurred on

your behalf that is foreign earned income included in your gross

income for the tax year (without regard to section 911).

Examples of employer-provided amounts are the following.

•

Wages and salaries received from your employer.

•

The fair market value of compensation provided in kind (such

as the fair rental value of lodging provided by your employer as

long as it isn't excluded on line 25).

•

Rent paid by your employer directly to your landlord.

•

Amounts paid by your employer to reimburse you for housing

expenses, for educational expenses of your dependents, or as

part of a tax equalization plan.

Self-employed individuals. If all of your foreign earned income

(Part IV) is self-employment income, skip lines 34 and 35 and

enter -0- on line 36. If you qualify for the housing deduction, be

sure to complete Part IX.

Part VII

Married couples. If both you and your spouse qualify for, and

choose to claim, the foreign earned income exclusion, figure the

amount of the exclusion separately for each of you. You each

must complete Part VII of your separate Forms 2555.

Limit on Housing Expenses Worksheet—Line 29b

Keep for Your Records

Note. If the location in which you incurred housing expenses isn't listed in the table at the end of these instructions, and the number of days

in your qualifying period that fall within the 2023 tax year is 365, DO NOT complete this worksheet. Instead, enter $36,000 on line 29b.

1. Enter the number of days in your qualifying period that fall within the 2023 tax year. (See the

instructions for line 31.) .............................................................. 1.

2. Did you enter 365 on line 1?

No. If the amount on line 1 is less than 365, skip line 2 and go to line 3.

Yes. Locate the amount under the column Limit on Housing Expenses (full year) from the table at

the end of these instructions for the location in which you incurred housing expenses. This is your

limit on housing expenses. Enter the amount here and on line 29b. Also, see Election to apply

higher limit on housing expenses, later.

STOP

Do not complete the rest of this worksheet ........................................

2.

3. Enter the amount under the column Limit on Housing Expenses (daily) from the table at the end of

these instructions for the location in which you incurred housing expenses. If the location isn't listed in

the table, enter $98.63. Also, see Election to apply higher limit on housing expenses, later .......... 3.

4. Multiply line 1 by line 3. This is your limit on housing expenses. Enter the result here and

on line 29b ........................................................................ 4.

Instructions for Form 2555 (2023)

-5-

Page 6 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Community income. The amount of the exclusion is not

affected by the income-splitting provisions of community

property laws. The sum of the amounts figured separately for

each of you is the total amount excluded on a joint return.

Part VIII

If you claim either of the exclusions, you can't claim any

deduction, credit, or exclusion that is definitely related to the

excluded income. If only part of your foreign earned income is

excluded, you must prorate such items based on the ratio that

your excludable earned income bears to your total foreign

earned income. See

Pub. 54 for details on how to figure the

amount allocable to the excluded income.

The exclusion under section 119 and the housing deduction

are not considered definitely related to the excluded income.

Line 44. Report in full on Schedule 1 (Form 1040) and related

forms and schedules all deductions allowed in figuring your

adjusted gross income (Form 1040, line 11). Enter on line 44 the

total amount of those deductions (such as the deductible part of

self-employment tax, and the expenses claimed on Schedule C

(Form 1040)) that aren't allowed because they are allocable to

the excluded income. This applies only to deductions definitely

related to the excluded earned income. See

Pub. 54 for details

on how to report your itemized deductions that are allocable to

the excluded income.

Line 45. Enter the amount from line 45 on Schedule 1 (Form

1040), line 8d. Reduce the other items of additional income by

the negative amount on line 8d and enter the total on Schedule 1

(Form 1040), line 9.

Enter the amount from line 10 of Schedule 1 (Form 1040) on

line 8 of Form 1040 or 1040-SR. If line 10 of Schedule 1 (Form

1040) is a negative number, enter it on line 8 of Form 1040 or

1040-SR in parentheses. Reduce the total of lines 1 through 7 of

Form 1040 or 1040-SR by this amount before reporting total

income on line 9 of Form 1040 or 1040-SR.

Part IX

If line 33 is more than line 36 and line 27 is more than line 43,

complete this part to figure your housing deduction.

Line 49. Use the Housing Deduction Carryover

Worksheet—Line 49 to figure your carryover from 2022.

1-year carryover. If the amount on line 46 is more than the

amount on line 47, you can carry the difference over to your

2024 tax year. If you cannot deduct the excess in 2024 because

of the 2024 limit, you cannot carry it over to any future tax year.

Housing Deduction Carryover Worksheet—Line 49

Keep for Your Records

1. Enter the amount from your 2022 Form 2555, line 46 .......................................

1.

2. Enter the amount from your 2022 Form 2555, line 48 .......................................

2.

3. Subtract line 2 from line 1. If the result is zero, stop; enter -0- on line 49 of your 2023 Form 2555. You do

not have any housing deduction carryover from 2022 ....................................... 3.

4. Enter the amount from your 2023 Form 2555, line 47 .......................................

4.

5. Enter the amount from your 2023 Form 2555, line 48 .......................................

5.

6. Subtract line 5 from line 4 .............................................................

6.

7. Enter the smaller of line 3 or line 6 here and on line 49 of your 2023 Form 2555. If line 3 is more than

line 6, you cannot carry the difference over to any future tax year ............................. 7.

-6-

Instructions for Form 2555 (2023)

Page 7 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

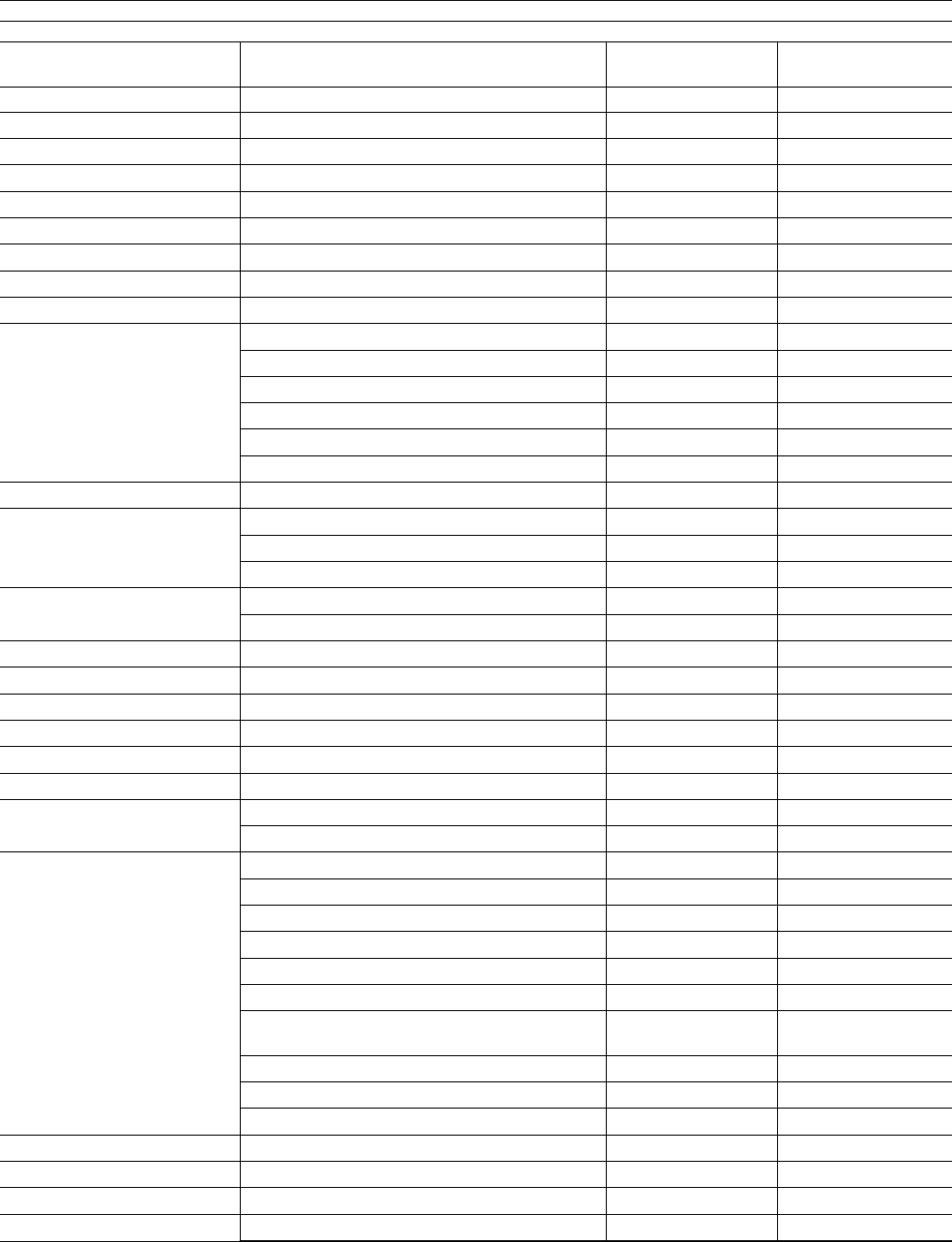

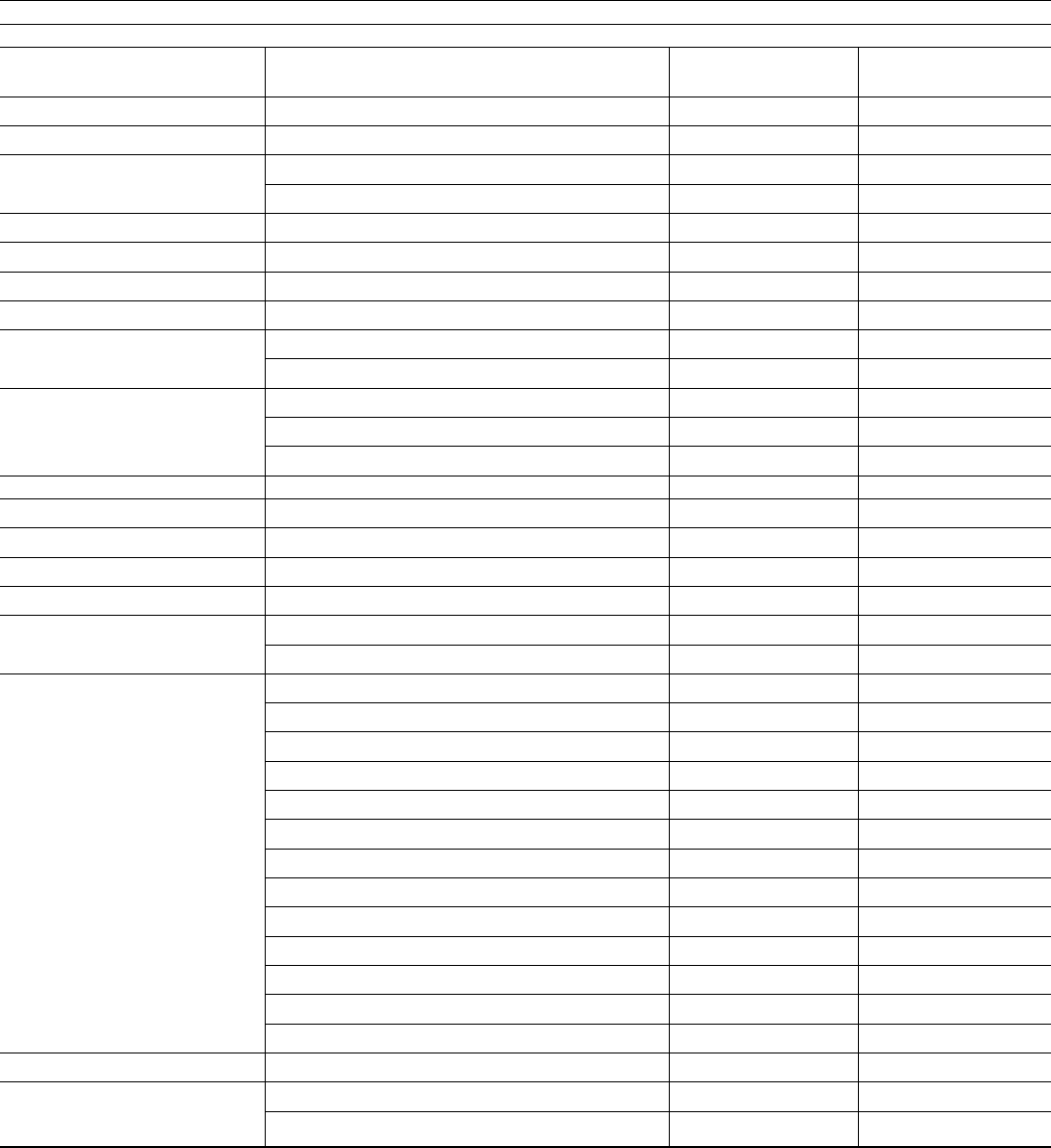

2023 LIMITS ON HOUSING EXPENSES

Country City or Other Location

Limit on Housing

Expenses (daily)

Limit on Housing

Expenses (full year)

. .

Angola Luanda 230.14 84,000

Argentina Buenos Aires 154.79 56,500

Australia Sydney 182.19 66,500

Bahamas, The Nassau 136.16 49,700

Bahrain Bahrain 132.33 48,300

Barbados Barbados and Bridgetown 103.29 37,700

Belgium Brussels 106.03 38,700

Bermuda Bermuda 246.58 90,000

Brazil Sao Paulo 155.07 56,600

Canada Calgary 105.75 38,600

Montreal 144.11 52,600

Ottawa 126.30 46,100

Toronto 164.11 59,900

Vancouver 155.62 56,800

Victoria 113.15 41,300

Cayman Islands Grand Cayman 131.51 48,000

China Beijing 190.68 69,600

Hong Kong 313.15 114,300

Shanghai 156.17 57,001

Colombia Bogota 160.82 58,700

All cities other than Bogota 135.34 49,400

Costa Rica San Jose 103.56 37,800

Democratic Republic of the Congo Kinshasa 115.07 42,000

Denmark Copenhagen 119.74 43,704

Dominican Republic Santo Domingo 124.66 45,500

Ecuador Quito 104.66 38,200

Estonia Tallinn 127.67 46,600

France Garches, Paris, Sevres, Suresnes, and Versailles 181.92 66,400

Lyon 100.55 36,700

Germany Berlin 109.04 39,800

Boeblingen, Ludwigsburg, Nellingen, and Stuttgart 108.49 39,600

Bonn 115.07 42,000

Cologne 153.97 56,200

Gelnhausen and Hanau 112.33 41,000

Ingolstadt 127.40 46,500

Kaiserslautern, Landkreis, Pirmasens, Sembach, and

Zweibrueken 109.32 39,900

Mainz and Wiesbaden 121.92 44,500

Munich 127.40 46,500

Wahn 115.07 42,000

Guatemala Guatemala City 115.07 42,000

Guinea Conakry 140.55 51,300

Holy See, The Holy See, The 121.10 44,200

India Mumbai 186.08 67,920

Instructions for Form 2555 (2023)

-7-

Page 8 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2023 LIMITS ON HOUSING EXPENSES

Country City or Other Location

Limit on Housing

Expenses (daily)

Limit on Housing

Expenses (full year)

India (cont.) New Delhi

153.76 56,124

Indonesia Jakarta 103.50 37,776

Ireland Dublin 105.21 38,400

Israel Beer Sheva 158.90 58,000

Jerusalem 134.25 49,000

Tel Aviv 139.18 50,800

West Bank 134.25 49,000

Italy Genoa 114.52 41,800

La Spezia 110.68 40,400

Milan 180.82 66,000

Naples 124.11 45,300

Rome 121.10 44,200

Vicenza 101.10 36,900

Jamaica Kingston 112.88 41,200

Japan Gifu, Komaki, and Nagoya 203.56 74,300

Okinawa Prefecture 129.32 47,200

Osaka-Kobe 248.39 90,664

Tokyo 210.96 77,000

Yokohama 112.33 41,000

Yokosuka 121.37 44,300

Kazakhstan Almaty 131.51 48,000

Korea Camp Colbern 148.49 54,200

Camp Market, K-16, Kimpo Airfield, Seoul, and Suwon 133.15 48,600

Camp Mercer 148.49 54,200

Kuwait Kuwait City 176.44 64,400

All cities other than Kuwait City 158.08 57,700

Luxembourg Luxembourg 99.18 36,200

Malaysia Kuala Lumpur 126.58 46,200

Malta Malta 150.96 55,100

Mexico Merida 103.84 37,900

Mexico City 131.23 47,900

All cities other than Ciudad Juarez, Cuernavaca,

Guadalajara, Hermosillo, Matamoros, Mazatlan,

Merida, Metapa, Mexico City, Monterrey, Nogales,

Nuevo Laredo, Tijuana, and Veracruz

107.95 39,400

Mozambique Maputo 108.22 39,500

Netherlands Amsterdam and Schiphol 144.93 52,900

Aruba 107.67 39,300

Hague, The 144.38 52,700

Netherlands Antilles Curacao 125.48 45,800

Oman Muscat 113.15 41,300

Panama Panama City 108.22 39,500

Peru Lima 107.12 39,100

Poland Warsaw 137.53 50,200

Portugal Alverca and Lisbon 110.68 40,400

-8-

Instructions for Form 2555 (2023)

Page 9 of 9 Fileid: … ions/i2555/2023/a/xml/cycle04/source 13:16 - 16-Oct-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

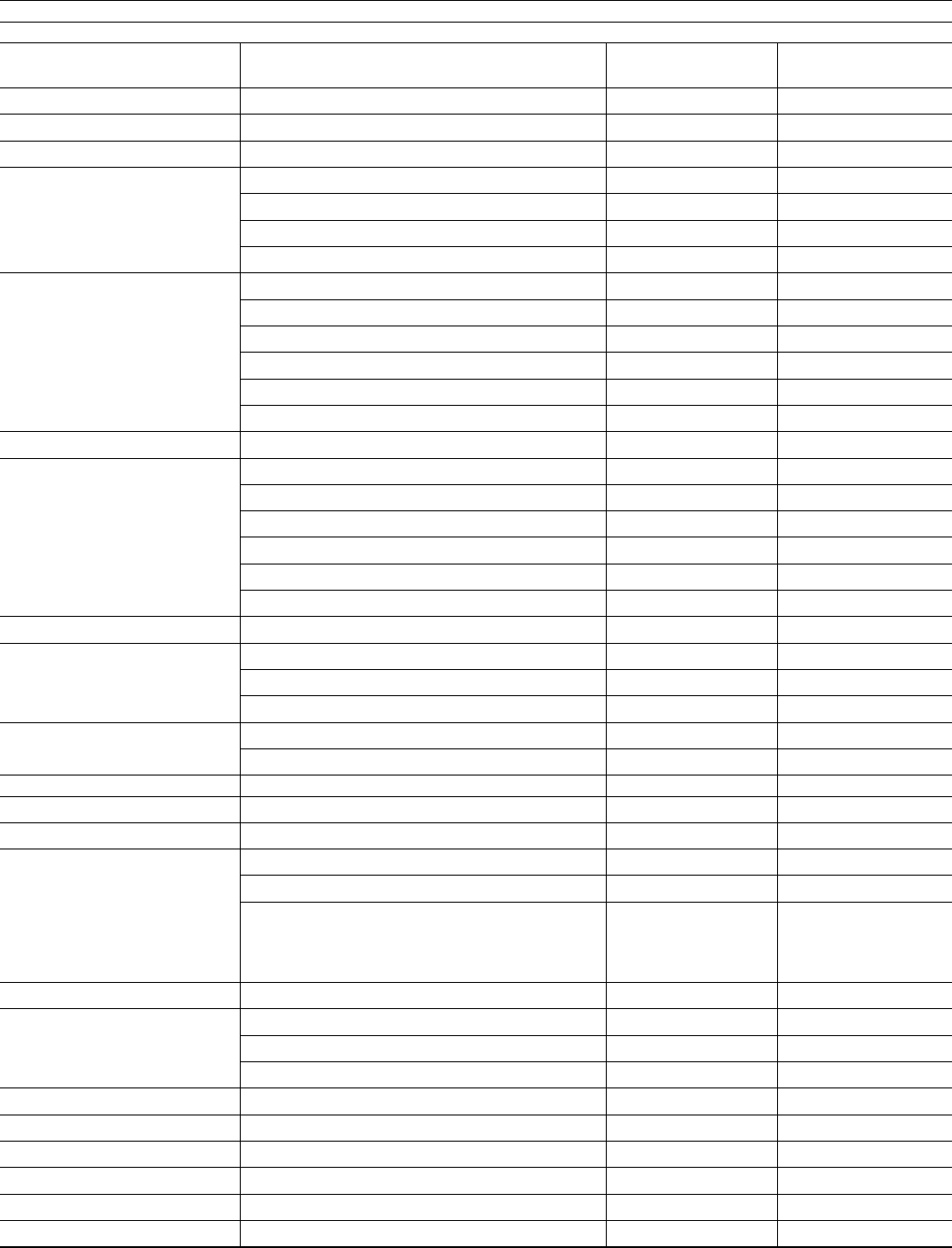

2023 LIMITS ON HOUSING EXPENSES

Country City or Other Location

Limit on Housing

Expenses (daily)

Limit on Housing

Expenses (full year)

Qatar Doha 125.72 45,888

Romania Bucharest 112.88 41,200

Russia Moscow 295.89 108,000

Saint Petersburg 164.38 60,000

Saudi Arabia Riyadh 109.59 40,000

Singapore Singapore 227.12 82,900

Slovenia Ljubljana 127.12 46,400

South Africa Pretoria 107.67 39,300

Spain Barcelona 111.23 40,600

Madrid 147.67 53,900

Switzerland Bern 189.04 69,000

Geneva 269.32 98,300

Zurich 107.45 39,219

Taiwan Taipei 126.54 46,188

Tanzania Dar Es Salaam 120.55 44,000

Thailand Bangkok 161.64 59,000

Trinidad and Tobago Port of Spain 149.32 54,500

Ukraine Kiev 197.26 72,000

United Arab Emirates Abu Dhabi 136.13 49,687

Dubai 156.64 57,174

United Kingdom Basingstoke 112.60 41,099

Bath 112.33 41,000

Bracknell, High Wycombe, and Reading 170.14 62,100

Caversham 202.19 73,800

Cheltenham 124.93 45,600

Farnborough 149.86 54,700

Felixstowe 94.25 34,400

Gibraltar 122.24 44,616

Lakenheath and Mildenhall 116.71 42,600

London 176.99 64,600

Loudwater 143.56 52,400

Southampton 121.10 44,200

Surrey 132.61 48,402

Venezuela Caracas 156.16 57,000

Vietnam Hanoi 128.22 46,800

Ho Chi Minh City 115.07 42,000

Instructions for Form 2555 (2023)

-9-